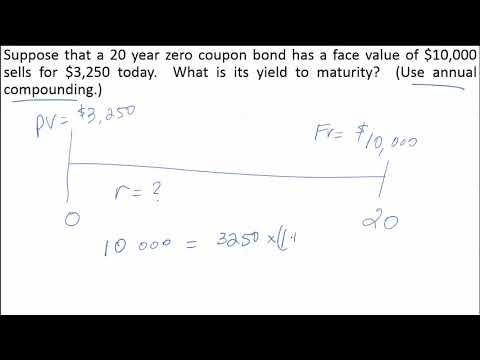

39 yield to maturity of zero coupon bond

Yield to Maturity vs. Coupon Rate: What's the Difference? - Investopedia WebMay 20, 2022 · The yield to maturity (YTM) is the percentage rate of return for a bond assuming that the investor holds the asset until its maturity date. It is the sum of all of its remaining coupon payments. Bond maturity value calculator - cfc.atelierines.pl In the yield to maturity calculator , you can choose from six different frequencies, from annually to daily. In our example, Bond A has a coupon rate of 5% and an annual frequency. This means that the bond will pay $1,000 * 5% = $50 as interest each year. Determine the years to maturity The n is the number of years from now until the bond matures.

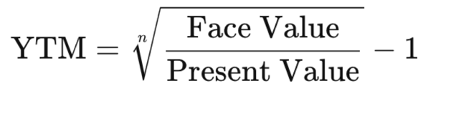

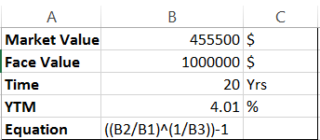

How to Calculate Yield to Maturity of a Zero-Coupon Bond Yield To Maturity=(Current Bond PriceFace Value)(Years to Maturity1)−1 Zero-Coupon Bond YTM Example Consider a $1,000 zero-coupon bond that has two years until maturity. The bond is currently valued at $925, the price at which it could be purchased today. The formula would look as follows: = ( 1000 925 ) ( 1 2 ) − 1

Yield to maturity of zero coupon bond

Bond Duration Calculator – Macaulay and Modified Duration WebWhere: Payment_x: The payout of the bond at point x; Par Value: The payout at maturity when the bond matures, or the par or face value; n: The total number of bond payouts in the future (assuming no missed payment) yield: The yield of the bond at point x (remember yields are often annualized, this yield must be adjusted for periods per year); Current … How do I Calculate Zero Coupon Bond Yield? - Smart Capital Mind The zero coupon bond yield is easier to calculate because there are fewer components in the present value equation. It is given by Price = (Face value)/ (1 + y) n, where n is the number of periods before the bond matures. This means that you can solve the equation directly instead of using guess and check. The yield is thus given by y = (Face ... Bond Yield: Definition, Formula, Understanding How They Work Aug 02, 2022 · The coupon yield — or coupon rate — is the interest you earn annually from a bond. For example, if you bought a bond for $100 and earned $5 in interest per year, that bond would have a 5% ...

Yield to maturity of zero coupon bond. Yield to Maturity (YTM) Definition & Example | InvestingAnswers The estimated YTM for this bond is 13.220%. How Yield to Maturity Is Calculated (for Zero Coupon Bonds) Since zero coupon bonds don't have recurring interest payments, they don't have a coupon rate. The zero coupon bond formula is as follows: Yield to Maturity Calculator Solved 15, A zero-coupon bond has a yield to maturity of 9% - Chegg Transcribed image text: 15, A zero-coupon bond has a yield to maturity of 9% and a par value of $1,000 if the bond matures in eight years, the bond should sell for a price of A. $422.41 B. $501.87 C. $513.16 D. $483 49 today 16. Yield to Maturity (YTM) - Investopedia WebMay 31, 2022 · Yield to maturity (YTM) is the total return anticipated on a bond if the bond is held until it matures. Yield to maturity is considered a long-term bond yield , but is expressed as an annual rate ... Zero Coupon Bond | Investor.gov Zero Coupon Bond. Zero coupon bonds are bonds that do not pay interest during the life of the bonds. Instead, investors buy zero coupon bonds at a deep discount from their face value, which is the amount the investor will receive when the bond "matures" or comes due. The maturity dates on zero coupon bonds are usually long-term—many don't ...

Zero-Coupon Bond Definition - Investopedia The interest earned on a zero-coupon bond is an imputed interest, meaning that it is an estimated interest rate for the bond and not an established interest rate. For example, a bond with a face... Zero Coupon Bond Value Calculator: Calculate Price, Yield to Maturity ... Calculating Yield to Maturity on a Zero-coupon Bond YTM = (M/P) 1/n - 1 variable definitions: YTM = yield to maturity, as a decimal (multiply it by 100 to convert it to percent) M = maturity value P = price n = years until maturity Let's say a zero coupon bond is issued for $500 and will pay $1,000 at maturity in 30 years. Yield curve - Wikipedia WebThe team extended the maturity of European yield curves up to 50 years (for the lira, French franc, Deutsche mark, Danish krone and many other currencies including the ecu). This innovation was a major contribution towards the issuance of long dated zero-coupon bonds and the creation of long dated mortgages. Zero coupon bonds are back in flavour. Will the party continue? WebSep 06, 2022 · The difference between the issue price and the maturity value of the zero coupon bond is the capital gain for the investor. ... The yield on these bonds ranged from 7.21 percent to 8.50 percent ...

Zero-coupon bond - Wikipedia A zero coupon bond (also discount bond or deep discount bond) is a bond in which the face value is repaid at the time of maturity. Unlike regular bonds, it does not make periodic interest payments or have so-called coupons, hence the term zero-coupon bond. When the bond reaches maturity, its investor receives its par (or face) value. Yield to Maturity (YTM) - Overview, Formula, and Importance On this bond, yearly coupons are $150. The coupon rate for the bond is 15% and the bond will reach maturity in 7 years. The formula for determining approximate YTM would look like below: The approximated YTM on the bond is 18.53%. Importance of Yield to Maturity Value and Yield of a Zero-Coupon Bond | Formula & Example - XPLAIND.com The bonds were issued at a yield of 7.18%. The forecasted yield on the bonds as at 31 December 20X3 is 6.8%. Find the value of the zero-coupon bond as at 31 December 2013 and Andrews expected income for the financial year 20X3 from the bonds. Value (31 Dec 20X3) =. $1,000. = $553.17. (1 + 6.8%) 9. Value of Total Holding = 100 × $553.17 ... Yield to Maturity Calculator | Calculate YTM The yield to maturity calculator (YTM calculator) is a handy tool for finding the rate of return that an investor can expect on a bond. As this metric is one of the most significant factors that can impact the bond price, it is essential for an investor to fully understand the YTM definition. ... In our example, Bond A has a coupon rate of 5% ...

2: Value of Zero-Coupon Bond Against Yield to Maturity ...

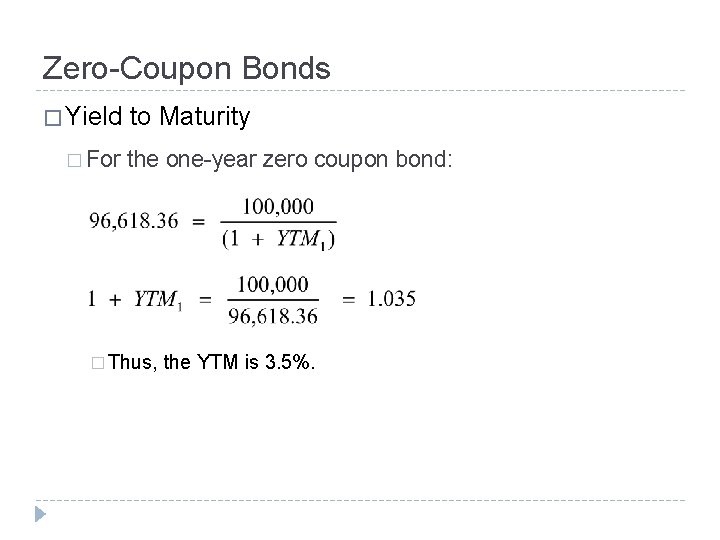

YIELDS TO MATURITY ON ZERO-COUPON RONDS - Ebrary Its yield to maturity is 5.174% (s.a.). The assumption of two periods in the year, while totally arbitrary, is common in financial markets because the yield on the zero then can be compared directly to yields to maturity on traditional semiannual payment fixed- income bonds.

What is a Zero Coupon Bond? Who Should Invest? | Scripbox

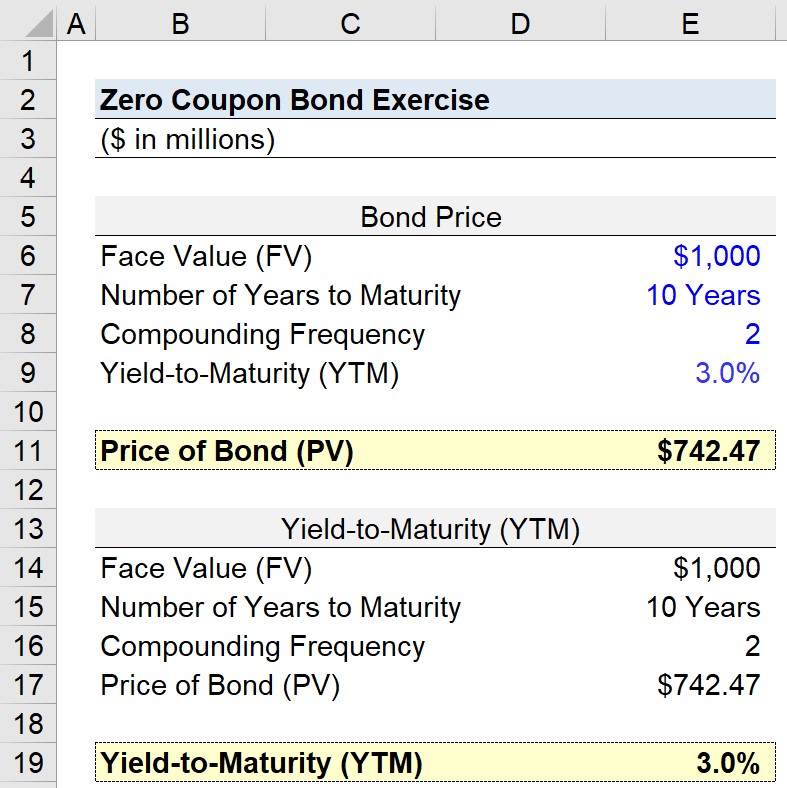

Zero-Coupon Bond: Formula and Calculator - Wall Street Prep Zero-Coupon Bond Yield-to-Maturity (YTM) Formula. The yield-to-maturity (YTM) is the rate of return received if an investor purchases a bond and proceeds to hold onto it until maturity. In the context of zero-coupon bonds, the YTM is the discount rate (r) that sets the present value (PV) of the bond’s cash flows equal to the current market price.

Solved] The following table shows some data for three zero ...

Calculate Price, Yield to Maturity & Imputed Interest for a Zero Coupon ... Instead interest is accrued throughout the bond's term & the bond is sold at a discount to par face value. After a user enters the annual rate of interest, the duration of the bond & the face value of the bond, this calculator figures out the current price associated with a specified face value of a zero-coupon bond.

LECTURE 09: MULTI-PERIOD MODEL BONDS

Zero-Coupon Bond - Definition, How It Works, Formula John is looking to purchase a zero-coupon bond with a face value of $1,000 and 5 years to maturity. The interest rate on the bond is 5% compounded semi-annually. What price will John pay for the bond today? Price of bond = $1,000 / (1+0.05/2) 5*2 = $781.20 The price that John will pay for the bond today is $781.20.

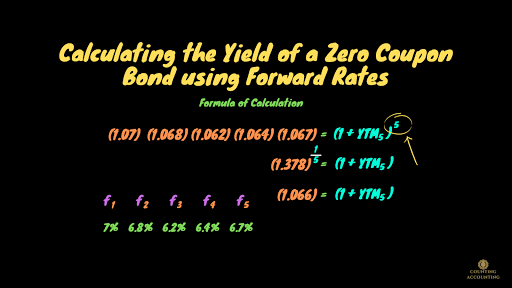

Calculating the Yield of a Zero Coupon Bond

Bond maturity value calculator - yzbuy.mptpoland.pl To calculate the current yield for a bond with a coupon yield of 4.5 percent trading at 103 ($1,030), divide 4.5 by 103 and multiply the total by 100. You get a current yield of 4.37 percent. Say you check the bond 's price later and it's trading at 101 ($1,010). last chance index splunk bungou stray dogs episode ...

Calculating the Yield of a Coupon Bond using Excel

Zero Coupon Bond - (Definition, Formula, Examples, Calculations) Web= $463.19. Thus, the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19. The difference between the current price of the bond, i.e., $463.19, and its Face Value, i.e., $1000, is the amount of compound interest Compound Interest Compound interest is the interest charged on the sum of the principal amount …

1-3.3. Bond Valuation: Zero-coupon Bonds - Module 1: Bond ...

Bond Pricing Formula | How to Calculate Bond Price? | Examples Webwhere C = Periodic coupon payment, F = Face / Par value of bond, r = Yield to maturity (YTM) and; n = No. of periods till maturity; On the other, the bond valuation formula for deep discount bonds or zero-coupon bonds Zero-coupon Bonds In contrast to a typical coupon-bearing bond, a zero-coupon bond (also known as a Pure Discount Bond or Accrual Bond) …

DOC) Chapter 16 Managing Bond Portfolios Multiple Choice ...

Yield to maturity - Wikipedia Then continuing by trial and error, a bond gain of 5.53 divided by a bond price of 99.47 produces a yield to maturity of 5.56%. Also, the bond gain and the bond price add up to 105. Finally, a one-year zero-coupon bond of $105 and with a yield to maturity of 5.56%, calculates at a price of 105 / 1.0556^1 or 99.47. Coupon-bearing Bonds

Zero Coupon Bond - (Definition, Formula, Examples, Calculations)

Bond Yield to Maturity (YTM) Calculator - DQYDJ Yield to Maturity of Zero Coupon Bonds. A zero coupon bond is a bond which doesn't pay periodic payments, instead having only a face value (value at maturity) and a present value (current value). This makes calculating the yield to maturity of a zero coupon bond straight-forward:

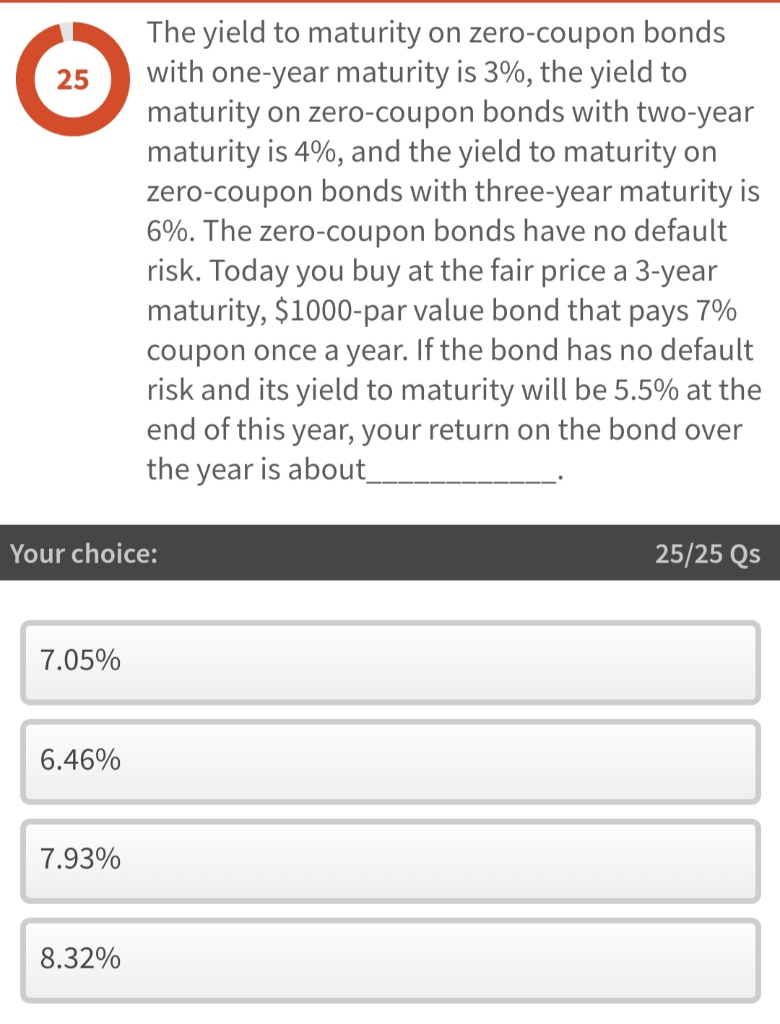

Solved 25 The yield to maturity on zero-coupon bonds with ...

Zero Coupon Bond Value - Formula (with Calculator) - finance formulas A 5 year zero coupon bond is issued with a face value of $100 and a rate of 6%. Looking at the formula, $100 would be F, 6% would be r, and t would be 5 years. After solving the equation, the original price or value would be $74.73. After 5 years, the bond could then be redeemed for the $100 face value.

What is a Zero Coupon Bond? Who Should Invest? | Scripbox

Bond Convexity Calculator: Estimate a Bond's Yield Sensitivity WebBond Price vs. Yield estimate for the current bond. Zero Coupon Bonds. In the duration calculator, I explained that a zero coupon bond's duration is equal to its years to maturity. However, it does have a modified (dollar) duration and convexity. Zero Coupon Bond Convexity Formula. The formula for convexity of a zero coupon bond is:

VALUING BONDS

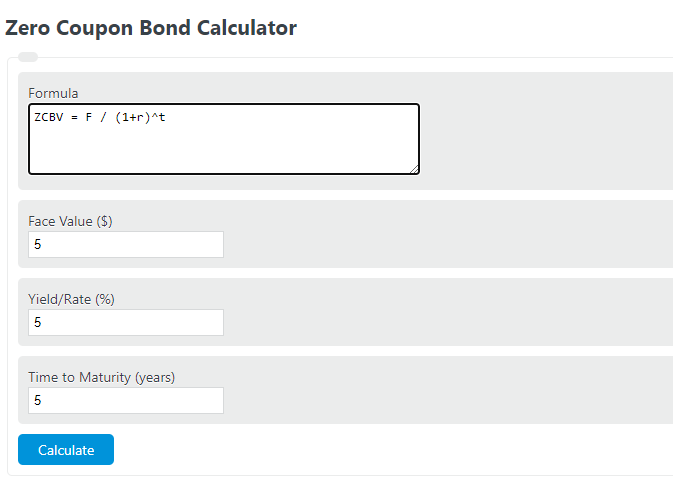

Zero Coupon Bond Calculator 【Yield & Formula】 - Nerd Counter In the given formula, the numeral of zero (0) represents that there is no coupon yet. Face Value (F) Rate/Yield (r) Time to Maturity (t) = When the term zero-coupon bond comes, the two words urgently come into mind; one is the pure discount bond, and the other one is the discount bond. Both of these words represent the common zero coupon bond term.

Solved The yield to maturity (YTM) on 1-year zero-coupon ...

What is the yield to maturity (YTM) of a zero coupon bond with a face ... Answer (1 of 2): YTM is 5.023%. Bond mathematics tend to be easier to calculate on a spreadsheet as seen below: Calculated the Yield first using RATE function. Parameters can be found out using the 'fx' button in MS Excel. You can see the parameters used in the above image as well viz. B6*B7 ->...

The yield to maturity (YTM) on 1-year zero-coupon bonds is 5 ...

Important Differences Between Coupon and Yield to Maturity - The Balance The yield increases from 2% to 4%, which means that the bond's price must fall. Keep in mind that the coupon is always 2% ($20 divided by $1,000). That doesn't change, and the bond will always payout that same $20 per year. But when the price falls from $1,000 to $500, the $20 payout becomes a 4% yield ($20 divided by $500 gives us 4%).

consider a coupon bond that has a 900 par value and a coupon rate of 6 the bond is currently selling

Bond Yield Calculator - CalculateStuff.com WebHow to Calculate Yield to Maturity. Yield to maturity (YTM) is similar to current yield, but YTM accounts for the present value of a bond’s future coupon payments. In order to calculate YTM, we need the bond’s current price, the face or par value of the bond, the coupon value, and the number of years to maturity.

How to Calculate the Yield of a Zero Coupon Bond Using ...

When is a bond's coupon rate and yield to maturity the same? Jan 13, 2022 · For example, if a company issues a $1,000 bond with a 4% interest rate, but the government subsequently raises the minimum interest rate to 5%, then any new bonds being issued have higher coupon ...

Zero Coupon bond Effective Yield to Maturity 1622 | Facebook

How to Calculate Yield to Maturity of a Zero-Coupon Bond - Investopedia Yield to maturity is an essential investing concept used to compare bonds of different coupons and times until maturity. Without accounting for any interest payments, zero-coupon bonds always...

Learn to Calculate Yield to Maturity in MS Excel

Zero Coupon Bond Yield - Formula (with Calculator) - finance formulas The formula for calculating the effective yield on a discount bond, or zero coupon bond, can be found by rearranging the present value of a zero coupon bond formula: This formula can be written as This formula will then become By subtracting 1 from the both sides, the result would be the formula shown at the top of the page. Return to Top

Zero Coupon Bond Calculator - Calculator Academy

Current yield - Wikipedia WebThe current yield, interest yield, income yield, flat yield, market yield, mark to market yield or running yield is a financial term used in reference to bonds and other fixed-interest securities such as gilts.It is the ratio of the annual interest payment and the bond's price: =. According to Investopedia, the clean market price of the bond should be the denominator in this …

Solved: A coupon bond pays annual interest, has a par value ...

How to Calculate a Zero Coupon Bond Price - Double Entry Bookkeeping As the face value paid at the maturity date remains the same (1,000), the price investors are willing to pay to buy the zero coupon bonds must fall from 816 to 751, in order from the return to increase from 7% to 10%. Bond Price and Term to Maturity The longer the term the zero coupon bond is issued for the lower the bond price will be.

Problem Set # 12 Solutions 1. A convertible bond has a par ...

Bond Yield: Definition, Formula, Understanding How They Work Aug 02, 2022 · The coupon yield — or coupon rate — is the interest you earn annually from a bond. For example, if you bought a bond for $100 and earned $5 in interest per year, that bond would have a 5% ...

Valuing Bonds Bond Cash Flows Prices and Yields

How do I Calculate Zero Coupon Bond Yield? - Smart Capital Mind The zero coupon bond yield is easier to calculate because there are fewer components in the present value equation. It is given by Price = (Face value)/ (1 + y) n, where n is the number of periods before the bond matures. This means that you can solve the equation directly instead of using guess and check. The yield is thus given by y = (Face ...

YIELDS TO MATURITY ON ZERO-COUPON RONDS

Bond Duration Calculator – Macaulay and Modified Duration WebWhere: Payment_x: The payout of the bond at point x; Par Value: The payout at maturity when the bond matures, or the par or face value; n: The total number of bond payouts in the future (assuming no missed payment) yield: The yield of the bond at point x (remember yields are often annualized, this yield must be adjusted for periods per year); Current …

Yield to maturity - Fixed income

MC algo 6-30 Zero Coupon Bond YTM There is a zero coupon bo ...

Zero-Coupon Bond - Definition, How It Works, Formula | Wall ...

6.2.1 Flashcards | Quizlet

Calculate the YTM of a Zero Coupon Bond

Zero Coupon Bond | Definition, Formula & Examples Video

/zero-couponbond_final-a6ec3618516a49c9a3654a1c79c9b681.png)

Zero-Coupon Bond Definition

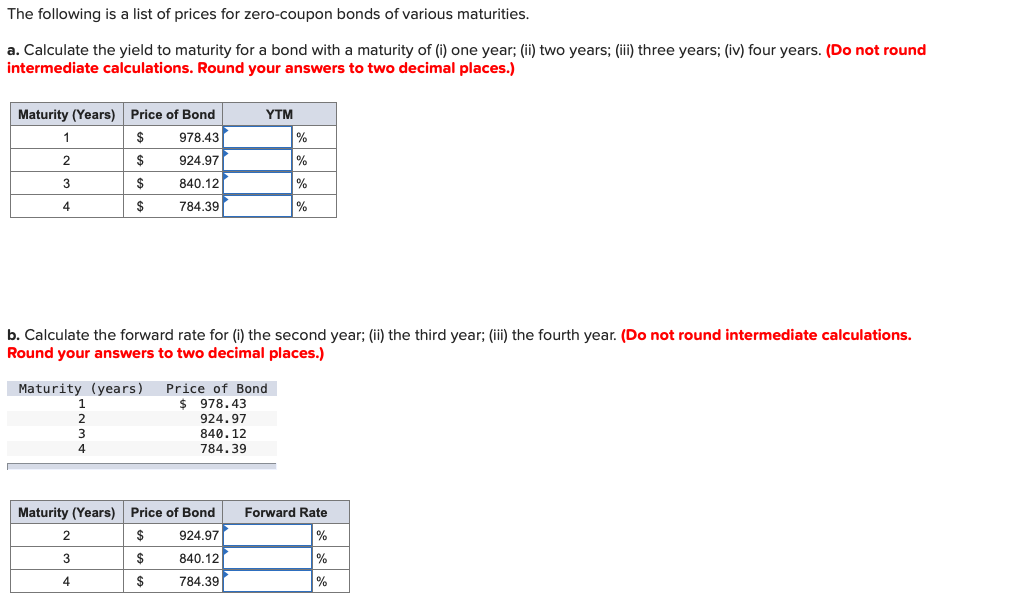

Solved The following is a list of prices for zero-coupon ...

Chapter 1

The Dummies Guide To Zero Coupon Bonds

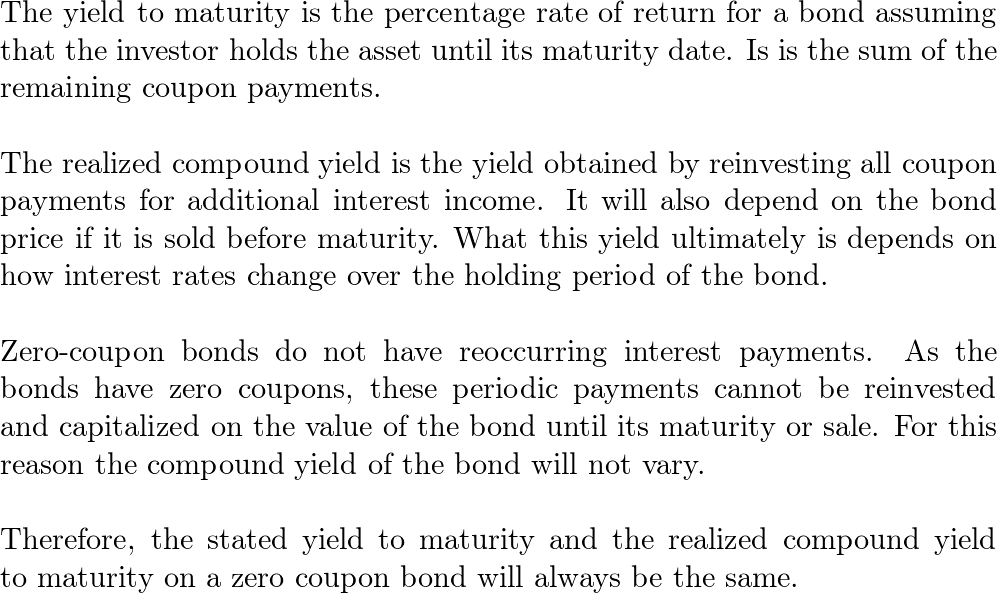

The stated yield to maturity and realized compound yield to ...

The Coupon Effect on Yield to Maturity

Chapter 7, interest rates and bonds - The possibility of a ...

Zero-Coupon Bond: Formula and Calculator

Zero-Coupon Bond: Formula and Calculator

WWWFinance - Bond Valuation: Campbell R. Harvey

Post a Comment for "39 yield to maturity of zero coupon bond"